JPMorgan Chase & Co

Company Snapshot & Price Performance

Source: Company data, Bloomberg, Alpha Vantage API

Recent Reported EPS

| Quarter | EPS | Quarter | EPS |

|---|---|---|---|

| Q4 25 | $4.63 | Q4 24 | $4.81 |

| Q3 25 | $5.07 | Q3 24 | $4.37 |

| Q2 25 | $4.96 | Q2 24 | $6.12 |

| Q1 25 | $5.07 | Q1 24 | $4.44 |

Recent Share Price Trend

Executive Summary

Investment Thesis

Diversified “Fortress” Franchise Drives Durable High ROE

JPMorgan’s broad-based business model, spanning consumer banking, commercial & investment banking, and wealth management, delivers stable, high returns on equity (ROE) through economic cycles. In 2025 the bank achieved a ~20% ROTCE (return on tangible common equity), well above peers (Bank of America ~14%, Goldman Sachs ~16%, Citigroup ~8% ROTCE). This reflects superior earnings power anchored by JPM’s “fortress balance sheet” strength and diversified revenue streams.

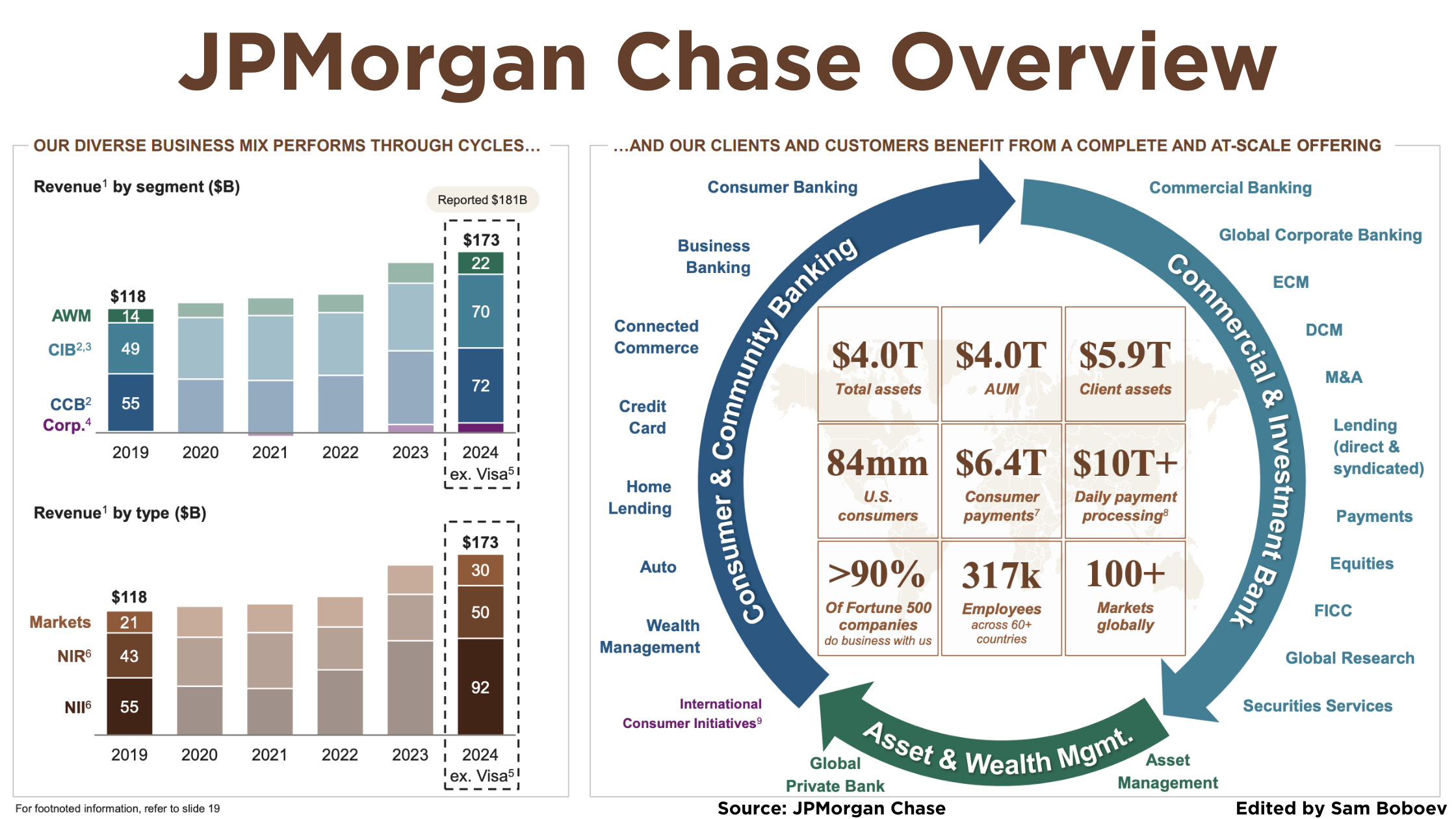

JPMorgan’s scale and balance across segments provide multiple earnings levers. Its Consumer & Community Banking arm (39.6% of 2024 revenue) and newly unified Commercial & Investment Bank (38.8%) contribute the majority of revenue, with the rest from Asset & Wealth Management (~12%). This mix creates resiliency – for example, softer lending margins can be offset by fee businesses (payments, trading or asset management). In 2024, the Corporate & Investment Bank (CIB) earned a record $70 billion revenue (18% ROE), while consumer banking added 1.7 million net new checking accounts and 10.4 million new credit card accounts, fueling future growth. JPM’s fortress balance sheet (CET1 capital 14.5%) and conservative risk practices enable it to expand market share during industry turmoil – notably, it gained ~$50 billion in deposits in Q1 2023 amid regional bank failures.

Investors often price JPMorgan in line with other banks, overlooking its outsized franchise quality. The market may underappreciate JPM’s ability to consistently produce above-peer ROE through prudent risk management and diversification. For instance, concerns about industry-wide net interest margin compression or credit normalization have weighed on bank valuations broadly, yet JPM’s earnings are buffered by its fee income streams and leading scale efficiencies (managed overhead ratio ~52% in mid-2025). The stock’s <10× P/E (on 2025 earnings) does not fully reflect JPM’s structural advantages, assuming it will merely perform like an average bank. We believe the market is undervaluing the durability of JPM’s earnings engine and its capacity to capitalize on sector disruptions (like winning deposit share or client assets during times of stress). In short, JPM’s franchise strength and balanced business model give it a quality premium that is not yet fully priced in.

Figure 1: JPMorgan’s diversified revenue base (2024) was split roughly 40% Consumer & Community Banking, 39% Commercial & Investment Bank, 12% Asset & Wealth Management, 9% Corporate/Other. This balance underpins stable overall performance, as growth or cyclical strength in one division can offset softness in another.

Figure 1: JPMorgan’s diversified revenue base (2024) was split roughly 40% Consumer & Community Banking, 39% Commercial & Investment Bank, 12% Asset & Wealth Management, 9% Corporate/Other. This balance underpins stable overall performance, as growth or cyclical strength in one division can offset softness in another.

Market Leadership Across Banking Verticals and Growth Initiatives Underappreciated

JPMorgan holds #1 or top-tier positions in virtually all its major businesses, from retail deposits to investment banking, positioning it to capture outsized growth as financial activity rebounds. The bank leads global investment banking with a 9.3% fee wallet share (ranked #1 in 2024 across M&A, debt and equity underwriting), and it is a top consumer bank with the largest U.S. deposit base (~$2.4 trillion). Ongoing strategic moves, including the acquisition of First Republic’s private banking franchise and the integration of the Apple Card portfolio, further extend JPM’s reach. This leadership translates to revenue growth opportunities and pricing power that the market has not fully credited.

JPMorgan’s expansive client base and product breadth create cross-selling and volume growth advantages. In investment banking, its strengthened Commercial & Investment Bank unit is capturing the full client continuum “from startups to multinationals”, yielding record deal advisory fees ($3.3 billion in 2024, 9.6% global share). Similarly, in consumer and wealth management, JPM is capitalizing on secular trends: it recorded $553 billion in net new client asset flows in 2025 – a testament to its appeal to affluent customers, bolstered by the First Republic acquisition (now expected to add ~$2 billion to annual revenue vs. $500 million initially forecast). The ongoing integration of the Apple Card (a two-year tech build) should modernize JPM’s card platform and eventually grow its card loans and fee income. Importantly, JPM’s sheer scale allows it to reinvest aggressively: it is boosting 2026 expenses by ~$9 billion (to ~$105 billion) largely to fund technology, AI and payments infrastructure, investments smaller peers struggle to match. These factors drive superior customer acquisition and product innovation, reinforcing JPM’s leadership moat.

The market appears to underplay JPMorgan’s capacity to outgrow the industry by gaining share. Skepticism around big-bank growth potential (and the law of large numbers) leads investors to assume JPM’s expansion will track the broader economy. However, recent results contradict this, e.g. JPM’s trading and deal revenues have been more resilient than peers, and its wealth management inflows are accelerating despite industry headwinds. The consensus may also be overly focused on legacy peer comparisons (e.g. viewing Goldman Sachs or Citigroup in the same light) without recognizing JPM’s unique execution (for instance, JPM successfully navigated consumer banking where Goldman retrenched). In essence, the market misprices JPM by not fully appreciating that its dominance in key verticals (and strategic acquisitions) can deliver above-market growth in revenues and client assets, rather than merely reflecting average industry trends.

Beneficiary of a Favorable Macro Outlook and Cyclical Tailwinds

Under JPMorgan’s base-case macro scenario for 2026 characterized by a soft landing economy with the Federal Reserve easing interest rates and stable credit conditions, the bank is positioned to benefit disproportionately. Management’s 2026 guidance assumes two Fed rate cuts (per the forward curve) alongside continued loan growth and only modest deposit runoff. In this environment, JPM can sustain robust net interest income (NII) around $103 billion while asset quality remains benign (2026 credit card charge-offs are expected at ~3.4%, consistent with a resilient consumer). A soft landing also likely revives capital markets activity, boosting JPM’s fee businesses. The bank’s mix of interest and non-interest revenue makes it a prime beneficiary of this Goldilocks macro backdrop.

Several cyclical tailwinds come into play for JPM:

Interest Rate Easing: As the Fed begins cutting rates, funding costs for banks should fall. JPM anticipates lower wholesale funding costs will add ~$8 billion to markets NII, roughly offsetting lower asset yields. With its industry-leading deposit base, JPM stands to stabilize net interest margin even in a declining rate scenario, as deposit betas normalize (rate cuts reduce pressure on depositors seeking higher yields).

Loan Growth and Credit Quality: The bank forecasts continued loan growth, particularly in cards, reflecting healthy consumer balance sheets. Unlike a recessionary scenario, the soft-landing outlook implies unemployment stays low, keeping credit losses manageable. JPM’s consumer data still shows no deterioration in charge-off trends.

Capital Markets & Investment Banking Upside: Constructive equity and debt markets in a stable-growth, lower-rate environment should spur deal-making. JPM has noted a strong 2026 investment banking pipeline with “constructive market dynamics”, expecting deal activity to rebound (some transactions were pushed from 2025 into 2026). As the #1 global IB, JPM is positioned to capture outsized fee growth when the cycle turns up. In sum, the base-case macro (moderating rates, growth not dropping off) provides multiple incremental tailwinds to JPM’s revenue and easing pressure on funding costs.

Investor sentiment remains cautious on banks due to macro uncertainty. Many fear either a sharp recession (bear case) or, conversely, that Fed rate cuts will crimp banks’ margins. This has created a valuation gap where JPM is not fully valued for a benign scenario. The market seems to price a downside skew (recession or stagflation) more than the likelihood of a soft landing. We believe this is a mispricing: JPM’s own outlook and balance sheet preparation cover a wide range of outcomes (management even stressed it’s ready for rates anywhere 2%–8% or even a recession), yet base-case conditions are favorable. Should inflation indeed ease and growth persist (as current consensus expects ~70–80% chance of soft landing), JPM’s earnings could surprise to the upside via higher fee momentum and controlled credit costs. The market underestimates how JPM’s flexibility (e.g. redeploying excess capital as regulations allow, or reversing loan loss reserves if losses remain low) could drive upside in a soft landing. Thus, investors have an opportunity to own a high-quality bank at a discount due to overblown macro fears, a normalization of sentiment in line with JPM’s base-case would likely catalyze a re-rating.

Technology & AI Leadership Unlocking Efficiency and New Revenue

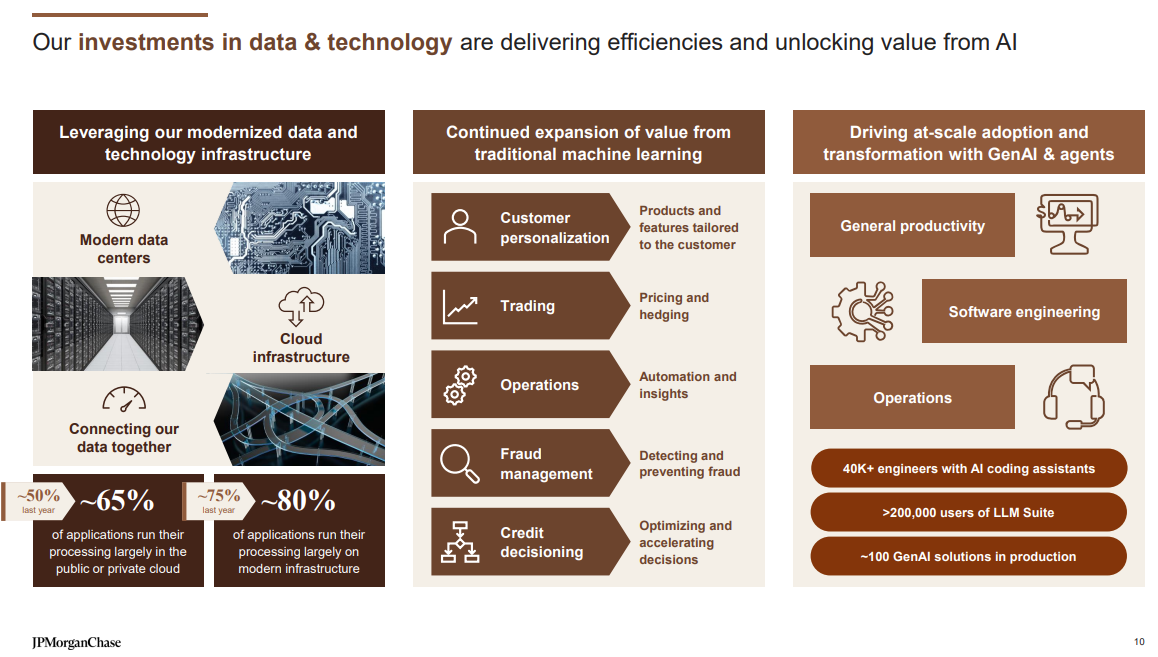

JPMorgan’s aggressive investment in technology, particularly artificial intelligence (AI) and digital platforms, is creating material competitive advantages in efficiency and product innovation that the market has yet to monetize. The firm already uses AI in over 400 use cases (from fraud detection to marketing analytics) and is actively expanding into generative AI to transform customer service and software development. JPM’s tech budget (~$15 billion+ annually, with 2026 tech spend up meaningfully) supports initiatives like its in-house large language model, new AI-driven investment products, and blockchain-based payments. Over time, these should lower costs and generate new fee streams, boosting JPM’s structural profitability beyond current expectations.

Several tangible developments illustrate JPM’s tech leadership:

AI-Enabled Operations: JPMorgan’s proprietary AI tools are already delivering efficiency gains. For example, the COiN platform (Contract Intelligence) uses machine learning to review loan contracts, reportedly saving 360,000 hours of legal work annually (virtually eliminating human error in that process). Similarly, advanced AI-driven fraud detection systems help reduce losses by spotting anomalies faster than manual review. These kinds of AI deployments in back-office and risk functions improve the bank’s cost structure (lower non-interest expense per unit of asset) and enhance risk management. Generative AI for Employees: In 2024 JPM launched “LLM Suite,” a ChatGPT-like internal chatbot, to ~50,000 employees in asset and wealth management. This large language model assists staff with research, idea generation and document summarization – essentially doing parts of a junior analyst’s work. Early adoption in wealth management suggests it boosts productivity and client responsiveness (e.g. quicker investment recommendations or customized reports). Rival banks (e.g. Morgan Stanley) have taken similar steps, but JPM’s firm-wide scale of deployment signals it could reap efficiency gains sooner by freeing up employee capacity for higher-value tasks.

New AI-Driven Products: JPMorgan is also innovating on the revenue side using AI. Notably, it unveiled “IndexGPT,” an AI-powered tool that creates thematic investment indexes using OpenAI’s GPT-4 model. IndexGPT can rapidly analyze trends (e.g. cloud computing, e-sports) by scanning news and identifying related companies, automating the creation of index products. This capability enables JPM to offer clients bespoke thematic portfolios at scale, tapping into the boom in personalized investing. It exemplifies how JPM can monetize AI by packaging it into new services (in this case, index and ETF products) that drive fee income. Additionally, JPM’s ongoing work in digital assets and blockchain (e.g. tokenized deposits and payments via JPM Coin) is another tech-forward avenue that could open new markets or cost savings.

Many investors treat big banks’ tech spend as a drag on near-term earnings rather than a value-creator, perhaps due to skepticism about incumbents competing with fintechs. In JPM’s case, this translates into an undervaluation of the long-term payoff from its tech leadership. The market may be missing a few key points: First, JPM’s tech investments have historically yielded tangible results (for instance, its digital banking apps helped drive record customer acquisition, and its trading systems give it share gains in markets). Second, the bank’s embrace of AI is likely to flatten its efficiency curve, even as others struggle with high overhead, JPM’s expense growth is increasingly tied to “good expense” on innovation that should eventually lower the cost-to-income ratio. Third, new AI-enabled products (like AI-driven advisory, or improved personalization in banking) can differentiate JPM and justify premium pricing or market share gains. Because these benefits are somewhat abstract or longer-term, the stock doesn’t yet reflect them. We believe this is a mispricing: over the next 1–3 years, evidence of AI-driven margin improvement or new revenue (such as faster index product growth from IndexGPT, or lower fraud losses) will lead the market to assign greater value to JPM’s tech-savvy franchise. In short, JPMorgan’s tech and AI strategy represents a hidden asset that is not fully embedded in consensus forecasts or valuation, offering upside as it materializes.

Business Model & Economics

JPMorgan Chase is the largest U.S. bank, with a universal banking model spanning retail banking, commercial banking, investment banking, and asset management. The firm serves over 60 million American households and many of the world’s top corporations. Its Consumer & Community Banking segment (Chase) offers retail services (deposits, loans, credit cards, payments, and wealth advice to mass-affluent clients). The Commercial & Investment Bank segment provides a full suite of wholesale banking: commercial lending, treasury services, investment banking (M&A advisory, equity/debt underwriting), and markets activities (trading and market-making across fixed income, equities, etc.). JPM is a top-two player in both consumer banking (by deposits) and investment banking (by fees). The Asset & Wealth Management division manages money for institutions and high-net-worth individuals, with over $3 trillion in assets under management. JP Morgan’s business model is often described as a “financial supermarket,” but critically it is managed in an integrated way, cross-selling products across divisions (e.g. offering a business founder both M&A advice and personal private banking). This breadth provides diversified revenue: in 2024, consumer banking contributed~$71.5B, the CIB $70B, and AWM $21.6B. Such diversity insulates JPM’s overall earnings from any single segment’s volatility. Furthermore, JPM operates with a “fortress” balance sheet: as of end-2025 it had $3.9 trillion in assets funded by a large deposit base (~$2.5 trillion+) and a strong capital position (CET1 ~14.5% vs. ~12% regulatory requirement). This enables the bank to lend and market-make at scale while comfortably meeting regulatory stress tests.

Unit Economics

JPMorgan’s unit economics benefit from economies of scale and low funding costs. A core driver is net interest margin on its loans and securities, which is enhanced by the firm’s massive base of low-cost deposits (many of which are checking and savings accounts with modest interest rates). During the 2022–2023 rising rate cycle, JPM had an influx of deposits (flight-to-quality) and was able to keep deposit betas (pass-through of rate hikes to depositors) relatively moderate, supporting NII of $85B in 2024 and an expected $95B ex-markets in 2026. Each incremental dollar of deposit is particularly valuable – it can be lent out or invested at the prevailing interest rate spread, so scale directly lowers JPM’s marginal funding cost per loan. On the lending side, JPM’s credit discipline maintains respectable risk-adjusted returns: for instance, in the card business, interest yields compensate for a normalized ~3–3.5% net charge-off rate, yielding attractive spreads. The bank’s fee businesses have high operating leverage as well, trading and investment banking revenues are largely earned on a fixed cost base (technology, personnel), so JPM’s leading volumes translate to strong incremental margins. Overall, JPMorgan runs efficiently for its size: in 2025 its managed overhead (expense-to-revenue) ratio was ~55%, which is best-in-class among big banks. Notably, management is intentionally reinvesting some of that efficiency back into growth (hence expenses are guided up to $105B in 2026). Even so, unit economics per customer remain attractive: a single Chase retail customer might have a checking account (near-zero cost of funds for JPM), a credit card (yielding ~12–15% interest on balances), and use Chase’s payments app (generating interchange fees), collectively, lifetime value of a multi-product customer is high relative to acquisition cost. Similarly, a mid-sized corporate client might use JPM for loans, cash management, and bond underwriting; the incremental cost to serve an additional product is low due to integrated platforms. These dynamics show up in superior profitability metrics, e.g. ~20% ROTCE in 2025 far above the cost of capital, indicating that JPM earns an economic profit on its activities at the margin.

Economic Moat

JPMorgan’s moat stems from scale, breadth, and brand, all reinforced by technological prowess. As the largest U.S. bank, JPM enjoys scale economies that few competitors can match: it spreads billions in fixed costs (technology investments, compliance, branch networks) over a huge revenue base, resulting in lower unit costs. This scale is hard for smaller banks or fintechs to replicate, especially under rising regulatory costs. Additionally, JPM’s breadth of services creates a network effect: clients benefit from a one-stop-shop (for example, corporations can rely on JPM for everything from daily cash management to complex capital markets deals), which increases switching costs. The firm’s deep client relationships often span decades, contributing to an intangible reputational moat. JPM’s brand, fortified by trust in its stability (enhanced after it was seen as a safe haven in 2023’s regional bank crisis), makes it a default choice for many customers. Moreover, JPMorgan’s risk management culture and “fortress balance sheet” philosophy act as a moat in volatile times: competitors that falter (Bear Stearns, WaMu in 2008; First Republic in 2023) often leave JPM to inherit their clients. The technological lead is an increasingly important moat component: JPM spends more on tech (over $14B/year) than many fintech companies’ total revenue, allowing it to develop cutting-edge AI, digital platforms, and cybersecurity that smaller banks struggle to afford. This investment has tangible moaty effects, e.g. JPM’s mobile banking app and digital services consistently rank at the top, keeping younger customers within its ecosystem. In institutional services, the bank’s electronic trading and payments systems offer speed/reliability that attract volume (and thus liquidity pools competitors can’t easily steal). Finally, scale confers a funding advantage: JPM’s AA- credit rating and surplus deposit liquidity mean it can raise capital or borrow at lower rates than peers, undercutting others on pricing if needed. All these factors, brand trust, one-stop breadth, scale efficiency, and tech advantage, form a robust competitive moat. It would be extremely difficult for a new entrant (or even an existing competitor) to dislodge JPMorgan from its leadership position in the many markets it operates.

Industry & Competitive Landscape

Industry Structure & Secular Trends

The banking industry, especially in the U.S., is oligopolistic at the top with a long tail of smaller players. JPMorgan is part of the “Big Four” U.S. banks (with Bank of America, Citigroup, and Wells Fargo) that collectively hold a significant share of deposits and loans. These megabanks benefit from diversification and regulatory backing (often deemed systemically important). Meanwhile, regional and community banks compete on local relationships but lack scale for certain products. The industry structure has been evolving: post-2008 regulations initially curtailed risk appetite, but over the last decade, fintech and big tech entrants have started chipping at specific services (payments apps, peer-to-peer lending, robo-advisors, etc.). However, rather than displace major banks, many fintechs have partnered with or been acquired by them. A clear secular trend is digital transformation, consumers increasingly favor mobile banking and instant payments. Large banks like JPM have invested heavily here, while some smaller banks fell behind (leading to customer attrition). Another trend is consolidation: weak banks are getting absorbed (recent example: JPM acquiring First Republic in 2023, a fallout of niche overexposure). Regulators have been cautious about too much consolidation, but broadly the market share of top banks has inched up after each crisis. On the capital markets side, global investment banking has also concentrated towards U.S. bulge bracket firms (JPM, Goldman, etc.), especially as European banks retrenched after the eurozone crisis.

Secular forces affecting all banks

Technology & AI: Automation of processes and data analytics are changing how banks operate and compete (with JPM and peers pouring billions into AI, cloud, cybersecurity). Tech is also lowering barriers for customers to switch or multi-bank (e.g. fintech apps aggregating accounts), pressuring banks to innovate customer experience continually.

Consumer Behavior: Younger demographics expect seamless digital service; also there is growing preference for sustainable investing and financial inclusion, nudging banks to adapt product offerings.

Interest Rate Environment: After a long low-rate era, the sharp rise in rates in 2022–2023 was a stress test. Banks that managed duration risk well (JPM avoided major losses on its bond portfolio) fared better than those that didn’t (some regionals suffered large unrealized losses). Going forward, a normalization (rates easing gradually) is expected to benefit loan demand while relieving deposit pricing pressure.

Regulation: Post-2008, banks faced higher capital and liquidity requirements (Dodd-Frank, Basel III). Currently, proposals for even stricter capital rules (the “Basel IV” endgame) are a concern – big banks argue excessive capital could reduce lending. JPM’s CEO has been vocal that some rules are “duplicative… extremely costly” and may be reevaluated. We anticipate continued regulatory scrutiny, especially after 2023’s bank failures (e.g. more oversight on interest rate risk and uninsured deposits). That said, JPM and peers have the resources to comply, whereas smaller banks might struggle (potentially accelerating consolidation or niche exits).

Secular Growth Areas: Wealth management and private banking are growing as global wealth rises and big banks are expanding here (JPM’s huge 2025 inflows confirm the trend). Payments and transaction banking are also growing due to e-commerce and real-time payments adoption. A noteworthy long-term force is competition from non-banks: for instance, money market funds drew deposits away from banks in high-rate periods, and stablecoin issuers (if unregulated) could pose a threat to bank deposits. Banks are responding by lobbying for a level playing field and by entering those arenas (JPM’s tokenized deposits and Coinbase partnership in retail crypto show it’s “engaged” in new ecosystems). Overall, the industry is at an interesting juncture where traditional banking is blending with fintech innovation, and scale plus adaptability are key to thriving.

Competitive Positioning – JPMorgan vs. Key Peers

JPMorgan vs. Bank of America (BAC): Both are diversified megabanks with large retail and wealth businesses. JPM has pulled ahead on profitability (2025 ROTCE 20% vs. BAC’s ~4%) and investment banking clout. BofA’s strength lies in its massive deposit base (it led in U.S. retail deposits for years) and Merrill Lynch wealth unit. However, BofA has faced pressure from interest rate moves, it was more asset-sensitive and saw larger unrealized bond losses and deposit outflows when rates rose sharply. JPM navigated that environment better (actually growing deposits in early 2023 as customers left smaller banks). In technology, both spend heavily, but JPM is perceived as more innovative (e.g. BofA’s digital assistant Erica is a notable success, yet JPM’s adoption of AI is broader in scope with 400+ use cases). Both banks are positioning for a softer economy with resilient credit; BAC has slightly more consumer loan exposure to rate changes (e.g. mortgage book), whereas JPM’s mix of businesses is more balanced. We see JPM’s edge in execution and risk management as giving it a sustainable premium over BofA in returns and growth potential.

JPMorgan vs. Citigroup (C): Citigroup is a global bank but has been restructuring to focus on core businesses after years of underperformance. Citi’s 2025 ROTCE was below 10% ,roughly half of JPM’s, reflecting strategic and operational gaps. While Citi competes with JPM in corporate banking and trading (especially in fixed income, where Citi historically had strength), it lacks the robust U.S. consumer franchise that JPM enjoys. Citi is actually exiting most international consumer markets to simplify its operations. JPM, by contrast, has a thriving domestic consumer arm and is selectively international via its corporate and asset management businesses. In investment banking, Citi’s league table standings trail JPM’s (Citi is typically #3–#5 in global fees, versus JPM at #1). One area Citi outpaces is certain emerging markets presence, but JPM has been expanding globally as well (and often wins mandates due to its balance sheet and top credit ratings). Citi’s current strategy under new management is to improve efficiency and focus on institutional clients, a space where JPM is a formidable competitor. Essentially, JPMorgan is ahead on almost every metric: profitability, market share, technology, and investor confidence. The valuation gap (Citi trades near tangible book, reflecting skepticism, while JPM trades at a premium) underscores JPM’s superior positioning. We expect JPM to continue drawing high-value clients (and talent) from Citi and others until Citi’s turnaround, if successful, plays out over several years.

JPMorgan vs. Goldman Sachs (GS): Goldman is an interesting peer: a Wall Street powerhouse in investment banking and trading, but with a far smaller consumer footprint. Goldman’s revenues ($60B in 2025) and balance sheet (~$1.6T assets) are much smaller than JPM’s, and its business mix is more volatile (heavily tied to trading and deal cycles). Goldman attempted to diversify into consumer finance with its Marcus initiative and the Apple Card partnership, but those efforts stumbled (GS has since scaled back consumer ambitions, even offloading the Apple Card portfolio which JPM acquired). JPMorgan, by contrast, successfully spans both Wall Street and Main Street. In booming markets, Goldman’s pure-play model can deliver high ROE (it posted ~16% RoTE in 2025), but JPM’s steadier 15–20% ROE through cycles is arguably more valuable for a long-term investor. JPM also competes head-to-head with GS in investment banking: in 2024 JPM was #1 in M&A, ECM, DCM, overtaking Goldman in some categories. Goldman remains formidable in advisory and trading (often #1 in M&A historically), but JPM’s broad corporate relationships (stemming from lending and commercial banking ties) have helped it win deals that Goldman might not get. Moreover, JPM’s deep pockets allow it to invest in trading technology and risk-taking (balance sheet usage for clients) at a level Goldman can, but Goldman doesn’t have the cushion of stable consumer deposit funding. GS relies more on wholesale funding and has a higher cost of deposits when it tried retail, which is a disadvantage in a tight liquidity environment. Overall, JPM’s positioning relative to GS is as a more diversified, lower-risk-profile institution that can still capture Wall Street upsides. The trade-off is that Goldman might have more operating leverage to a roaring bull market, but JPM offers a superior risk-adjusted growth profile, especially with its successful integration of consumer finance and the largest U.S. retail bank at its core.

Other Competitors: Wells Fargo is another large U.S. bank, primarily domestic-focused like JPM/BofA. Wells has been constrained by regulatory asset caps and scandals, so it’s been losing ground – JPM likely absorbed some of that market share, particularly in deposits and perhaps mortgage lending where Wells was once #1. In asset & wealth management, JPM faces competitors like Morgan Stanley (which acquired E*Trade and Eaton Vance, and runs a large wealth business via Morgan Stanley Wealth Management and MS’s own asset management). Morgan Stanley has transformed into a more balanced firm (half wealth/asset management, half investment bank) and is a peer in serving high-net-worth clients. JPM’s edge there is its huge Chase client base funneling affluent individuals into its wealth products, plus the recently acquired First Republic private bank adds to that strength. In summary, JPMorgan stands at the apex of the industry – it is often the benchmark that other banks are compared against. Its challenge is to maintain this lead, but given scale and prudent management, it is well positioned to do so. Secular and cyclical trends (digitalization, globalization of wealth, etc.) seem to favor the biggest and best-capitalized banks, which bodes well for JPM’s continued dominance relative to both traditional peers and new entrants.

Catalysts & Timeline

Near-Term Catalysts (0-6 months)

Federal Reserve Easing Cycle

As the Fed potentially begins cutting interest rates in late 2025 or early 2026 (JPM’s base case assumes two rate cuts in 2026), investor sentiment toward banks could improve. Easing monetary policy would alleviate pressure on deposit costs and could steepen the yield curve, aiding bank margins. Additionally, rate cuts signal a more accommodative economic outlook, which may boost loan demand and reduce fears of credit stress – a net positive for JPM’s valuation.

Rebound in Capital Markets Activity

There are signs that investment banking pipelines are rebuilding (JPM noted deals deferred to 2026 and “strong client engagement” in its outlook). Any pickup in IPOs, M&A, or debt issuance in the coming quarters would directly boost JPM’s fee revenue. For example, a marquee tech IPO wave or large acquisition deals closing in 2025 would showcase JPM’s deal-making prowess and provide upside to consensus earnings.

Expense Discipline/Operating Leverage Evidence:

In the near term, JPM has guided for higher expenses (up to $105B in 2026). If over the next few quarters management demonstrates operating leverage – for instance, delivering earnings beats by controlling core expenses or proving that revenue lifts (from rates or fees) outpace expense growth – it would assuage concerns about profitability dilution. Any commentary that portions of tech spend are driving tangible savings (e.g. headcount efficiencies from AI) or new business would also be catalytic to the stock’s narrative.

Regulatory Relief or Clarity:

near-term wildcard catalyst is regulatory news. If regulators soften proposed capital rule changes or give banks an extended timeline to comply, it could buoy bank stocks. JPM in particular, with excess capital, could resume larger share buybacks if it gets clarity that capital buffers aren’t being overly tightened. Conversely, if anticipated rules (like Basel IV implementation) turn out less onerous than feared, that would remove a valuation drag. JPM’s CEO Jamie Dimon has been actively advocating for rational regulation.

Medium-Term Catalysts (6-18 months)

AI and Digital Monetization Milestones:

Over the medium term, we expect JPMorgan to launch AI-enhanced products to clients, which can act as catalysts as they gain traction. For example, the roll-out of the IndexGPT thematic investing tool in 2025–2026 could open a new revenue line (through ETF products or advisory services built on it). Similarly, if JPM introduces a consumer-facing AI financial advisor (leveraging its internal LLM capabilities), it could attract significant new assets or deposits. Investor perception will shift positively if JPM can demonstrate that its AI investments are not just cutting costs but also growing top-line via better client acquisition or wallet share. We will watch for KPI disclosures such as: number of clients using AI-driven features, efficiency ratio improvements attributed to AI, or revenue uplift in segments where AI is deployed.

Market Share Gains in Key Segments

Medium-term catalysts include observable shifts in market share that validate JPM’s strategy. In wealth management, for instance, continued outsized net inflows (building on the record $0.5 trillion+ in 2025) would signal JPM pulling away from peers as a go-to wealth manager. In investment banking, maintaining the #1 rank and possibly extending fee market share towards 10%+ globally (from 9.3% in 2024) would confirm JPM’s dominance. These gains could come as European banks retreat or if boutiques lose ground in a bigger deal environment – any league table published showing JPM at the top in M&A or underwriting can be a catalyst for investor confidence (often reflected in relative valuation premiums). On the consumer side, watch for deposit growth resumption: if and when industry deposit outflows (to money markets) subside as rates fall, JPM’s huge acquisition of new accounts (1.7M new checking in 2025) puts it in pole position to grow core deposits again. A return to positive deposit growth (above industry average) in 2026 would be a strong bullish signal.

Efficiency Improvement and Profitability Targets

By 2027, JPM has an implicit target to return its expense growth to a more normalized level after this tech investment cycle. Medium term, as major projects (like Apple Card tech rebuild) conclude, the bank should begin to harvest efficiency gains. A catalyst will be if JPM can drive its overhead ratio back down in the low-50s% or even high-40s% while still growing revenue – essentially demonstrating scale efficiencies. Achieving (or beating) an ROTCE sustainably above, say, 17%+ in the medium term (excluding one-time items) would likely warrant a re-rating of the stock. Management often gives medium-term outlooks at Investor Day – any explicit efficiency or profitability targets set (and met early) could catalyze investor enthusiasm. For instance, if in Investor Day 2025 they project double-digit EPS growth through 2027 driven by operating leverage, and subsequent results track that, it would support multiple expansion for JPM.

Rising Capital Return (Dividends/Buybacks)

JPM has been cautious with share buybacks in 2023–2024 given uncertainty and acquisitions, but its capital generation is enormous (2025 net income was $57.5B). In the medium term, if credit stays benign and regulators finalize rules, JPM will likely resume substantial capital returns. A catalyst could be announcements of large share repurchase authorizations or dividend hikes beyond current levels. If JPM is able to return, say, $15B+ per year to shareholders without hurting growth – thanks to its earnings power – that will attract long-term investors and could be reflected in the share price. Especially once the First Republic goodwill and Apple Card RWA impacts are digested, JPM could find itself over-capitalized in a stable environment and choose to up its payout. Any signals in that direction (for example, a lower targeted CET1 ratio or commentary like “we have no M&A needs, capital will be returned”) would be a medium-term catalyst.

Macroeconomic “Soft Landing” Confirmation

Our thesis leans on a soft landing; tangible confirmation of this scenario would be catalytic for bank stocks and JPM in particular. If by mid-2026 it’s clear the economy avoided a recession – evidenced by steady GDP growth, unemployment remaining low ~4–5%, and inflation back in control – the narrative around banks could shift from fear of cycle peak to confidence in a prolonged benign cycle. That shift could narrow the valuation discount currently seen in bank stocks. For JPM, confirmation would show up in credit metrics (no spike in defaults), continued loan growth, and solid consumer spending data (management already cites resilient spend). Essentially, time passing without the shoe dropping on credit will itself be a catalyst: each quarter of normal performance in 2025–2026 increases the market’s comfort to award JPM a higher multiple more in line with its historical average (and in line with other high-ROE companies).

Valuation Analysis

Our DCF model values JPMorgan Chase & Co at $404.81 per share, representing a 28.6% upside to the current market price of $314.85.

Valuation Bridge

Revenue Growth Trajectory

Growth moderates from 9.1% to 5.4% as company matures, converging to long-term 3.3% terminal rate.

EBIT Margin Forecast

EBIT margins average 17.9% across forecast period, reflecting stable operational efficiency.

Key Operating Assumptions

| Assumption | Value |

|---|---|

| Capex as % of Revenue | 1.0% |

| D&A as % of Revenue | 2.0% |

| NWC Change as % of Revenue Δ | 2.0% |

| Cash Tax Rate | 20.8% |

Terminal Value

| Perpetual Growth Rate | 3.25% |

| Terminal Value | $1473.3B |

| % of Enterprise Value | 113.1% |

Terminal value assumes 3.25% perpetual growth, in line with long-term GDP expectations.

Sensitivity Analysis: Intrinsic Value per Share

Impact of changes in WACC and terminal growth rate on valuation (base case: $404.81)

| WACC ↓ / Growth → | 2.3% | 2.8% | 3.3% | 3.8% | 4.3% |

|---|---|---|---|---|---|

| 5.37% | $561.73 | $667.43 | $823.05 | $1074.90 | $1552.18 |

| 5.87% | $475.56 | $550.60 | $654.31 | $807.01 | $1054.14 |

| 6.37% | $410.33 | $466.08 | $539.72 | $641.50 | $791.35 |

| 6.87% | $359.24 | $402.10 | $456.82 | $529.09 | $628.98 |

| 7.37% | $318.14 | $351.99 | $394.07 | $447.77 | $518.70 |

Blue cell indicates base case valuation.Green = upside scenarios,Red = downside scenarios.

Valuation Methodology

The DCF model employs a Free Cash Flow to the Firm (FCFF) approach, valuing JPMorgan Chase & Co based on cash flows available to all capital providers. The methodology includes:

- Explicit Forecast Period (5 years): Operating performance projected based on management guidance, historical trends, and industry dynamics.

- Terminal Value: Represents value beyond the explicit forecast, calculated using perpetuity growth at 3.25%. Accounts for 113.1% of total enterprise value.

- Discount Rate: All cash flows discounted at WACC of 6.37%, reflecting the company's cost of capital and risk profile.

- Bridge to Equity Value: Enterprise value adjusted for net debt ($156.6B) to derive equity value attributable to common shareholders.

Bull & Bear Cases

Bull Case

Bull Case (from DCF model)

Target: $452.00 per share (+43.6% vs current $314.85)

| Metric | Bull Case |

|---|---|

| Intrinsic Value/Share | $452.00 |

| Enterprise Value | $1436.26B |

| WACC | 6.05% |

Assumptions: Higher revenue growth, margin expansion, lower discount rate.

Bear Case Scenario

Bear Case (from DCF model)

Target: $277.80 per share (-11.8% vs current $314.85)

| Metric | Bear Case |

|---|---|

| Intrinsic Value/Share | $277.80 |

| Enterprise Value | $943.11B |

| WACC | 6.79% |

Assumptions: Lower growth, margin pressure, higher discount rate.

Justification

While our long thesis is confident, we acknowledge several key risks that could impair JPMorgan’s performance. We outline these risks alongside mitigation factors and the potential bear case scenario.

Bear Case

Macro Downturn (Recession)

The biggest risk is a sharp economic downturn (a hard landing) that diverges from JPM’s base-case. If inflation remains high or geopolitical shocks hit, the Fed could keep rates higher-for-longer and possibly tip the economy into a recession. In a bear-case recession scenario (e.g. 2026 sees unemployment spike well above 6% and GDP contract), JPM’s earnings would face pressure on multiple fronts: credit losses would surge (consumer defaults in cards and business loan delinquencies would require large reserve builds), loan growth would stall or reverse, and fee revenues from investment banking would likely dry up. The combination could cause JPM’s net income to drop significantly (historically in severe recessions, big bank profits can fall 30–50% or even swing to a loss if the downturn is extreme). For instance, JPM’s credit card net charge-off rate could overshoot the ~3.4% expected to, say, 5–6% in a deep recession, while corporate defaults could trigger losses in the investment bank.

Mitigation: JPMorgan’s fortress balance sheet provides substantial loss-absorbing capacity. The bank carries over $37 billion in loan loss reserves (as of end-2025) and a CET1 capital ratio of 14.5%, giving it a cushion to absorb shocks. Management runs regular stress tests – notably, they plan capital assuming an adverse scenario – and has stated “There’s no scenario where capital is gonna be the issue”. In practice, JPM would likely remain profitable even in a moderate recession (albeit with lower earnings), and its dividend, backed by strong capital, would likely be maintained. Also, JPM’s diversified business means that certain areas (trading, for example) might outperform during volatility, offsetting some loan losses. Importantly, JPMorgan’s risk management (e.g. tighter underwriting standards in recent years, limited subprime exposure) and use of macro hedges (interest rate hedges, credit derivatives) can blunt the impact. The bear case is largely about severity, a mild recession is within JPM’s planning and would be navigated; a severe financial crisis-style downturn, while low probability, is the scenario where the thesis would face the greatest challenge. In that extreme case, the mitigation is that JPM has historically gained share coming out of crises (it can purchase distressed competitors or simply use its strength to win customers when others fail). Nevertheless, a bad recession would delay the thesis, compress near-term returns, and likely hurt the stock (as bank valuations correlate with credit cycles). This is a risk we monitor via leading indicators (e.g. corporate default rates, consumer debt service ratios) and note that JPM’s own data currently shows resilience in consumer finances.

Regulatory and Policy Risk

As a globally significant bank, JPM faces constant regulatory oversight and the potential for adverse policy changes. Current looming risks include higher capital requirements – U.S. regulators have proposed implementing Basel III “endgame” rules that could raise risk-weighted assets or capital charges for large banks. If JPM is forced to hold substantially more capital, its ROE will mechanically decline (more equity for the same earnings). There’s also talk of stricter liquidity rules or limits on certain activities (like concentration limits, or additional TLAC debt requirements). Another angle is political risk: large bank profits and scale could become a target (e.g. windfall taxes in some jurisdictions, or limits on mergers which could cap growth).

Mitigation: JPMorgan is proactive in regulatory compliance and lobbying. Jamie Dimon has openly argued for a sensible recalibration of rules to avoid harming competitiveness. The bank is currently well-capitalized relative to requirements – CET1 of 14.5% vs. a required ~12.5% (including buffers) – meaning it has headroom to absorb higher requirements by adjusting payouts rather than drastically shrinking business. In anticipation of Basel IV, JPM has been optimizing assets (for example, shedding low-return risk-weighted assets, and integrating operations to reduce duplication of capital usage). The firm’s scale also lets it absorb compliance costs better than smaller peers. Additionally, if regulations tighten across the board, JPM’s relative position might strengthen (weaker banks would be hit harder, possibly driving more business to JPM). Nonetheless, regulatory changes could constrain upside – our thesis assumes no draconian increase that makes banking fundamentally less profitable. We are watching developments like the Fed’s capital framework review; clarity by late 2025 could actually be a catalyst if outcomes are milder than feared, but the opposite (stringent rules) is a risk that could trim JPM’s future returns.

Competition & Technological Disruption

JPM operates in highly competitive markets, not just versus traditional banks, but increasingly against fintech firms, Big Tech companies, and even non-bank alternatives (like bond funds or blockchain finance). A risk is that new technologies or business models erode parts of JPM’s moat. For example, payment innovation is fierce: fintechs enabling instant payments or central bank digital currencies could reduce banks’ cut of transactions. Large tech firms (Apple, Google, Amazon) have made inroads in payments and consumer finance (Apple’s credit card, Amazon lending to merchants, etc.), sometimes in partnership with banks but potentially as future competitors. Another disruptive threat is if decentralized finance (DeFi) or stablecoins attract substantial deposits away from banks – JPM’s CFO noted up to $6 trillion of bank deposits could be at risk long-term if stablecoins aren’t regulated.

Mitigation: JPMorgan’s strategy has been to embrace and lead in technology rather than ignore it. The bank has its own blockchain and tokenization initiatives (e.g. JPM Coin for wholesale payments, tokenized money market funds) to ensure it remains relevant in new financial architectures. It has partnered where sensible – e.g. linking with Coinbase to allow retail crypto access within Chase, so that if customers want digital assets, they need not leave JPM. The bank’s massive tech budget also means it can replicate or acquire fintech capabilities (as seen with its 2021 acquisition of OpenInvest and 55ip for digital investing tools, or building real-time payment Zelle functionality). Importantly, JPM’s brand and trust factor serve as a moat against newcomers: individuals and companies often prefer a well-capitalized, regulated institution for their life savings or large transactions (the 2023 deposit flight to JPM showed trust’s value). So even as fintechs innovate, JPM often ends up integrating those innovations (it’s telling that Apple chose a bank partner and now that portfolio sits with JPM). On pricing, competition (like higher deposit rates offered by online banks or money funds) is a risk to margins, but JPM’s diversified product set allows it to compete on more than price (bundling services, offering credit convenience, etc.). In summary, while tech disruption is a real risk, JPM’s approach to “disrupt itself” with heavy investment and its scale partnerships should mitigate being left behind. The risk to monitor is if we see major client defections or margin erosion in a segment due to a new competitor – so far, JPM’s growth in deposits and assets suggests it’s holding its own.

Execution Risk in AI/Tech Initiatives

We highlight JPM’s tech and AI investments as a positive, but there is risk in execution. Large-scale IT projects (like the Apple Card integration or building enterprise AI tools) can run over budget or under-deliver. If JPM spends $15B+ on tech and doesn’t realize commensurate benefits, it could weigh on efficiency and prove our thesis overly optimistic. For instance, AI deployment risk includes: the models might make errors (e.g. faulty advice to clients or biased decisions) leading to financial loss or reputational damage; data privacy issues could arise if AI inadvertently exposes sensitive information; or regulators might impose limits on AI usage in sensitive areas like credit underwriting, reducing potential gains. There’s also operational risk – cyber-security is critical as banks adopt more tech, and a major breach or outage at JPM could severely impact customer trust.

Mitigation: JPMorgan has a strong track record in large project execution (it successfully completed mergers like Bear Stearns, WaMu, and more recently the integration of First Republic’s systems is on track). The firm manages tech projects with disciplined oversight. For example, they are doing Apple Card integration over two years deliberately to get it right. On AI, JPM employs rigorous model validation and has governance in place (they won’t roll out generative AI to customers without thorough testing, currently internal use is sand-boxed for employees). They’ve also hired top talent and even created ethics boards for AI. We take some comfort that JPM’s leadership acknowledges both the promise and unknowns of AI – Dimon himself said the full effect and pace of AI are uncertain but potentially transformational, indicating the bank will remain flexible. As for cybersecurity, JPM is often cited as one of the most secure banks (with multi-hundred million annual cyber budget and state-of-the-art defense). No system is foolproof, but JPM has avoided any massive breaches to date, showing its controls are robust. In short, while execution missteps are possible (and we will keep an eye on expense trends and project updates), JPM’s scale and experience make it more likely to successfully implement these initiatives than many peers.

Franchise/Reputation Risk

Given JPM’s size and visibility, any scandal or significant compliance failure could damage its reputation and invite penalties. Banks have been fined for issues ranging from money-laundering control lapses to market manipulation in the past. JPM has generally navigated well, though it has paid fines (e.g. the London Whale trading incident in 2012). A future incident, say a major trading loss, or a high-profile legal case, is a tail risk that could hurt investor confidence.

Mitigation: The firm’s culture under Dimon emphasizes risk awareness and doing first-class business in a first-class way. They’ve invested in compliance and controls (JPM’s regulatory relationships are currently in good standing, with no significant outstanding consent orders unlike some peers). While one can’t predict unknown unknowns, JPM’s diversified approach means even a hit in one area (a trading loss, a legal fine) would be absorbed by the overall earnings power. Still, reputation takes years to build and moments to lose, so this remains a risk to consider, albeit not central to the thesis unless evidence emerges.

In a comprehensive bear case combining multiple adverse events, e.g. a recession hits in 2025 leading to surging credit losses, simultaneously the Fed keeps rates high squeezing margins, and regulators impose higher capital reducing ROE – JPM’s earnings could decline and its valuation (typically about 1.5–2.0× tangible book in good times) could drop toward 1× tangible book as investors fear a “new normal” of lower profitability. This could imply ~30–40% downside in the stock from current levels in a severe scenario. However, even in this bear case, JPMorgan’s fundamental solvency would likely not be in question; instead it would be a question of reduced returns. These risks can be weathered with time and resilience as JPM would use its earnings power to rebuild capital if needed, cut costs, and still likely emerge with stronger market share (as weaker competitors fall away). The bear case therefore is arguably a buying opportunity for a franchise like JPM, albeit painful in the short run. Nonetheless, as analysts, we must continuously evaluate these risks. At present, none of these risks appear outsized or unmanageable for JPM in light of its preparation and historical performance, which underpins our confidence in the long-term investment thesis.

Key Risks

Faster-than-expected NII normalization (rates, deposit betas, balance-sheet mix)

If rates fall sharply or deposit costs rise faster than asset yields reprice, NII could undershoot guidance and compress profitability.

Regulatory capital tightening reduces capital return / constrains growth

A more punitive capital framework could reduce buybacks and force balance-sheet reshaping at lower returns.

Credit cycle downturn (consumer + CRE/wholesale pockets)

A recessionary shock could lift losses (especially cards) and pressure provisioning and returns.

AI & Data Strategy

JPMorgan Chase has positioned itself at the forefront of AI adoption in banking, integrating artificial intelligence across the enterprise to enhance operations and create new client offerings. The bank’s approach to AI is two-pronged: internal efficiency (using AI to streamline processes, reduce costs, and improve risk management) and client-facing innovation (developing AI-driven products and services that can generate revenue or deepen customer engagement). Crucially, JPM’s scale allows it to gather vast datasets (transactions, customer interactions, market data) that fuel powerful AI models, and its hefty tech budget funds both in-house development and partnerships with leading AI firms.

AI in Operations and Risk Management

Internally, JPMorgan leverages AI and machine learning to automate and improve a wide array of processes. A flagship example is the COiN (Contract Intelligence) platform, which employs AI to review and interpret legal documents, notably commercial loan contracts, in seconds, a task that previously consumed 360,000 hours of lawyers’ and credit officers’ time each year. COiN not only slashes costs but also cuts errors to near-zero, illustrating AI’s impact on back-office productivity. Similarly, AI-driven algorithms are used in fraud detection and cybersecurity: JPM’s systems scan millions of transactions daily to flag anomalies that human eyes might miss, helping prevent fraud losses and cyber intrusions in real-time. The firm’s risk management has also benefited from machine learning models that better predict credit defaults or operational risks by analyzing patterns in historical data; this improves loan underwriting and capital allocation decisions. These uses of AI in operations contribute to JPM’s strong efficiency metrics (as noted, ~52% overhead ratio) by either reducing manual workload or by allowing the bank to handle higher volumes without proportional headcount increases. Importantly, JPM’s adoption of AI in risk areas is coupled with human oversight – for instance, if an AI model flags an unusual trading pattern as potential rogue behavior, compliance teams review it promptly. This symbiosis of AI and human expertise is a deliberate strategy to gain the best of both – speed and accuracy from algorithms, plus judgment and accountability from employees.

AI-Driven Products and Services

On the client-facing side, JPMorgan is actively exploring AI to enhance customer experience and generate new revenue streams. A notable development is IndexGPT, the AI-driven investment index platform the bank unveiled, which uses OpenAI’s GPT-4 to create thematic stock baskets. This tool automates the process of identifying companies related to an investment theme by analyzing news and data via NLP (natural language processing), enabling JPM to launch innovative index products much faster than traditional research methods. For clients, this means access to cutting-edge thematic investments (for example, a basket of “metaverse” stocks or “green energy” companies dynamically maintained by AI). JPM could package these indexes into ETFs or structured notes, thereby directly monetizing the AI capability. In retail banking, AI is improving personalization: JPM’s mobile app uses machine learning to provide tailored insights to customers (like forecasting bills or suggesting savings tips based on individual behavior). The bank has also been testing virtual assistants, akin to Alexa or Siri, within its banking apps. In fact, JPMorgan’s CEO has hinted at deploying AI chatbots for customer service, which could handle routine inquiries (“What’s my balance?” or simple transactions) conversationally, improving response times and availability. Over time, such AI agents might upsell or cross-sell, e.g. if a customer’s spending pattern suggests they could save on interest, an AI might proactively recommend a debt consolidation loan. In wealth management, as mentioned, JPM gave its financial advisors and researchers an internal LLM Suite (ChatGPT-like chatbot) to assist in idea generation; one can envision a client-facing version in the future where clients themselves get an AI co-pilot for financial planning (under human advisor supervision). Additionally, JPMorgan’s push into blockchain and smart contracts intersects with AI, for instance, trading algorithms or smart order routing in markets can incorporate AI to execute trades more efficiently for clients. The net impact of these AI-driven services is intended to be stickier customer relationships (better service keeps clients from switching) and new sources of fee income (e.g. advisory fees on AI-curated portfolios, or simply higher volumes due to improved client engagement).

Figure 2: Illustrative Map of JPMorgan’s AI Deployments

Figure 2: Illustrative Map of JPMorgan’s AI Deployments

Impact on Financials and Operations

The cumulative impact of JPM’s AI strategy is expected to materialize in both improved operational leverage and incremental revenue. Cost-wise, AI and automation should gradually lower JPM’s non-interest expense as a percentage of assets or revenue, effectively bending the cost curve. Management has described rising tech spend as critical “good expense” that will secure future efficiency. For example, if COiN and similar tools free up thousands of employee hours, JPM can control compensation costs or repurpose staff to more value-added roles (instead of hiring new staff for growth areas). We’ve already seen evidence: despite volume growth, JPM’s headcount has grown slower than assets, partly due to tech efficiencies. On the revenue side, while it’s early, offerings like IndexGPT suggest JPM can capitalize on AI to differentiate its products. Even a few successful AI-enabled products could contribute meaningfully, consider that a popular ETF or index product can generate hundreds of millions in fees annually; if IndexGPT helps JPM launch the next $10B AUM fund because it spotted an emerging theme first, that’s a direct revenue win attributable to AI. Moreover, better customer service through AI (e.g. 24/7 instant responses via chatbot) could increase customer retention and thus lifetime value. There’s also a competitive positioning aspect: JPMorgan’s public emphasis on AI (Jamie Dimon calling its consequences “extraordinary… transformational”) may bolster its appeal to tech-savvy clients and even to investors who are assigning higher multiples to companies perceived as AI leaders.

However, JPM is also candid that AI’s full impact will unfold over years, and it is measuring progress carefully. We will monitor metrics such as: efficiency ratio improvements, any explicit cost savings from AI that management quantifies, growth in digital engagement metrics (e.g. what percent of service requests handled by AI), and new revenue contributions (management might highlight how many products or strategies were AI-generated). Notably, in the Q4 2025 earnings call, Jamie Dimon said AI is “not a big driver [yet]” of the bottom line, but will be a big driver over time, indicating JPM expects a ramp-up rather than an immediate windfall.

Limits and Risks of AI in Banking

Despite the enthusiasm, JPMorgan recognizes the limitations and risks of AI, treating its implementation with appropriate caution. One limitation is that AI models, especially generative ones, can produce errors or “hallucinations” – unacceptable in critical financial computations. Thus, JPM isn’t likely to let an AI alone make credit decisions or trading calls without human oversight and rigorous validation. There are also regulatory and ethical boundaries: data privacy laws constrain using personal data for AI without consent, and regulations (like FRB/OCC guidance) will likely require explainability in AI-driven credit models to avoid discrimination. JPM must ensure its AI does not introduce bias, for instance, in a mortgage approval algorithm – which could lead to compliance violations or reputational harm. The bank is likely building frameworks for AI governance, and might even work with regulators to shape appropriate guidelines. Another risk is cybersecurity: AI tools could be targeted by hackers (e.g. an AI model that has access to sensitive info might be manipulated). JPM’s strong cyber defenses are a mitigating factor, but the risk evolves as AI systems become integral. Additionally, from a strategic view, while AI lowers some barriers, it could also help competitors; the algorithms JPM deploys are not exclusive (other banks and fintechs also use machine learning, and open-source AI is proliferating). So JPM must continuously innovate to maintain an edge, AI advantage can be transient if not coupled with superior data or execution.

Conclusion

In summary, JPMorgan’s AI strategy is ambitious but grounded: deploy quickly but safely. The firm is already reaping some efficiency benefits (hundreds of thousands of hours saved, improved fraud loss rates, etc.) and laying the groundwork for AI-driven growth (with new client solutions like IndexGPT). Over our investment horizon, we expect AI to be a positive contributor to JPM’s ROE – aiding in keeping costs low even as the bank grows, and opening avenues for higher revenues per client. The key will be managing the transition: training employees to work with AI, protecting data, and aligning AI initiatives with clear business goals (not just tech for tech’s sake). So far, JPM’s execution on technology in the past (being a leader in online banking, credit card analytics, etc.) gives us confidence. AI, as Dimon analogized, could be as revolutionary as past industrial revolutions. JPMorgan is ensuring it is on the forefront of that revolution in finance. If successful, this will further widen the gap between JPM and lesser-equipped competitors, underpinning its long-term growth and profitability, and thus rewarding shareholders of this forward-thinking franchise.

Important Disclosures

This report has been prepared by St. George Capital for educational purposes only. It does not constitute investment advice or a solicitation to buy or sell securities. St. George Capital and its members may hold positions in the securities discussed. Past performance does not guarantee future results. Investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.